The Paradox of Choice

March 16, 2026 Leave a comment

Today when we can open a trading account in minutes using multitudes of apps on our smartphones, start a side hustle overnight, and invest in everything from mutual funds to crypto, it’s easy to assume that greater financial freedom leads to greater happiness and security. After all, classical economics taught us that more choice expands utility and that having more options allows individuals to maximise satisfaction according to their preferences.

However, paradoxically, the modern reality is quite the opposite. The very availability of multiple financial choices, from investment platforms and passive income streams to flexible careers, has made us more anxious, instead of more secure. This tension between freedom and fatigue is at the core of what psychologist Barry Schwartz famously called The Paradox of Choice, that when faced with too many options, people often experience paralysis, regret, and dissatisfaction. In the financial world, this paradox is amplified by behavioural biases, social pressures, and the illusion of control. The promise of ‘financial freedom’ is increasingly becoming a source of stress and decision fatigue.

At the core of neoclassical economics lies the assumption of the rational consumer, an individual seeking to maximise utility given available resources and information. In theory, having more options allows a person to reach a higher indifference curve, implying greater satisfaction. However, this theory assumes two conditions of perfect information and bounded rationality that modern life rarely satisfies. In reality, our capacity to process and evaluate financial information is limited. According to Nobel laureate Herbert Simon, bounded rationality doesn’t really exist as people settle for ‘good enough’ decisions given cognitive constraints.

When applied to financial decisions of choosing mutual funds, stocks, insurance policies, side gigs, or career shifts, the cognitive load of evaluating multiple dimensions (returns, risk, time, opportunity cost, tax impact, and ethical values) becomes overwhelming. And, eventually, this results in anxiety, procrastination, and in many cases, decision paralysis.

Behavioural economics has consistently challenged the rational agent model by introducing psychological realism. The ‘overchoice effect,’ as demonstrated in Sheena Iyengar and Mark Lepper’s famous “jam experiment” (formally published in 2000), found that too many options reduce the likelihood of making any decision at all, instead of motivating consumers.

Translating this into financial behaviour, investors today face an explosion of options:

- Thousands of mutual funds and ETFs, each claiming a unique advantage

- Multiple investment apps with different algorithms and influencers

- Gig economy trends from freelancing to affiliate marketing to AI content creation

- Cryptocurrencies, NFTs, index funds, and more

Every new choice promises empowerment but demands research, comparison, and ongoing monitoring. Instead of creating financial autonomy, it traps individuals in a constant state of vigilance, which is the fear of missing out (FOMO) combined with the fear of making the wrong call (FOBO). The result is not empowerment but exhaustion or decision fatigue. Each micro-decision (Should I invest this month? Which stock to pick? Should I switch careers or start a podcast?) depletes mental energy. Over time, this erodes not just financial confidence but emotional well-being.

Daniel Kahneman’s Prospect Theory helps explain why financial freedom can be anxiety-inducing. The theory suggests that people are loss averse as the pain of losing 100 rupees is psychologically twice as intense as the pleasure of gaining the same amount. In an environment overflowing with options, every choice implies multiple foregone alternatives. Every decision carries not just the risk of loss but the weight of opportunity cost. This constant mental simulation of missed opportunities amplifies anticipated regret, a core feature of financial anxiety. Ironically, the very flexibility that defines financial freedom multiplies the avenues for potential regret. The ideology of ‘financial freedom’ is closely tied to neoliberal individualism, which believes that individuals are solely responsible for their economic success or failure. The gig economy and self-investing culture are framed as the democratisation of opportunity, but in practice, they shift systemic risk from institutions to individuals.

In the past, financial security was linked to stable employment, pensions, and collective risk-sharing. Today’s economy glorifies personal agency: ‘be your own boss,’ ‘invest smart, ‘create multiple income streams.’ This narrative sounds empowering, but simultaneously imposes a moral burden that if you are not financially thriving, it’s because you didn’t hustle enough or make the right investments. Digital technology has magnified this paradox. Social media and fintech apps blur the line between information and manipulation. Platforms gamify investing (colourful charts, animations, notifications) to keep users engaged. Influencers promote ‘hot’ stocks on popular social media or ‘passive income secrets’ that fuel financial comparison and insecurity.

The attention economy transforms finance from a domain of prudence into one of performance. People aren’t just managing money, instead they’re managing an identity. The psychological cost is immense and full of information overload, impulsive trading, and the erosion of long-term financial discipline. It is a proven fact that dopamine spikes from small gains, mimicking gambling behaviour, creating cycles of thrill and despair.

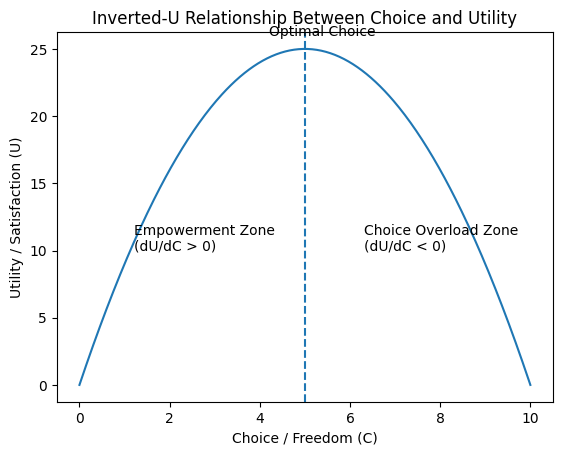

This anxiety can be visualised through diminishing marginal utility of choice. Initially, increasing options enhances utility as people enjoy flexibility. However, beyond a threshold, the utility curve flattens and then declines as cognitive costs exceed the benefits of freedom.

Mathematically, if U = f(C) represents utility derived from choice (C), then

for small C, dU/dC > 0 (freedom increases satisfaction),

for large C, dU/dC < 0 (freedom decreases satisfaction).

This inverted-U relationship illustrates that optimal well-being arises not from maximum freedom but from structured freedom, where choice is curated, meaningful, and bounded by context or expertise.

The paradox of financial choice reveals a deeper human truth that enjoying freedom without boundaries can be as imprisoning as constraint. The promise of financial autonomy has mutated into an obligation to constantly optimise, compare, and compete. It seems like we are drowning in option value as every unrealised choice weighs on our psyche. We are victims of decision fatigue as we are living through the privatisation of financial risk disguised as empowerment. True financial freedom, therefore, is not about multiplying options but mastering them and knowing when to choose, when to stop, and when to rest. As with most paradoxes, the solution lies in the balance of the freedom to simplify, ignore, and define what ‘enough’ means in a world that always demands more.

(Cover image is generated using AI)